Capital

United Homes Group's Roadmap To Becoming A Mega-Regional Giant

The Builder's Daily spoke at length with UHG President Jack Micenko on plans to acquire homebuilders in seven states in America's Southeast. Here are his top 10 insights.

At $10.3 billion in 2022 revenue on 22,000-plus home closings in operations in 35 metropolitan areas in 15 states plus the District of Columbia – and, arguably, the strongest track-record of shareholder returns and consolidated pre-tax profits in the business – there is only one NVR.

- it sets the standard so high for asset-light focus on process-driven per-home profitability that its inventory-turn rates might well be termed "asset lightning"

- its vertical construction operations, and vertically-integrated build-cycle management are widely regarded as second to none

- its team management training and talent cultivation are looked at as a homebuilding management academy, constantly growing the organization's bench strength even as it churns out entrepreneurs, leaders, and operators that thrive in other organizations

- its tighter than typical operating geography – with operations in the Northeast, Midwest, and Southeast – make NVR a mega-regional allowing it the competitive advantage of deeper scale and market dominance across its footprint.

No, there may not today be another enterprise the match of NVR. Nor might there ever be. That doesn't mean another organization can't borrow a page or two from the NVR playbook and wind up pretty damned successful in and of themselves. After all, remember, once upon a time not even NVR was NVR. It took 20 years and a near-extinction moment to evolve into the revered model of strategy, execution, and business culture it's become.

The strategic team at United Homes Group, homebuilding's freshman-year public company, would like, then, to get a move on in a bid to become America's second sustainable mega-regional public homebuilder. UHG's roots stretch back to 2004, when founder Michael Nieri was building homes out of his seriously decrepit pick-up truck and the bootstraps company was literally that.

Now, after a almost a two-decade build-learn-improve-rinse-and-repeat scale-up in South Carolina, Nieri's fluency in talent, trusted relationships, land strategy, building operations, and customer delight readied him for a go-big and go-bold play that – when it's fleshed out in the real world – may bear strong resemblance to none other than NVR.

Last week, we reported here the very first step UHG unveiled in a master strategy that envisions a Manifest Destiny radiating outward from the firm's Columbia, S.C.-based headquarters in every direction that there's land. We wrote:

United Homes Group announced this morning that by acquiring Raleigh-based Herring Homes, it's planting a flag in one of the U.S.'s top-20 new-home marketplaces, with opportunity to strike at as much as a third of the market's share of new-home real estate and construction business not already tied down by public and multi-regional private homebuilders clawing for their own deeper scale.

The move comes in a homebuilding and development business environment vibrating now with mergers and acquisitions courtships, particularly in America's domestic migration and regional economic growth magnets, adrenalized by emerging hybrid home-office workplace patterns, a flight to more-financially manageable costs-of-living, and equally strong desire for higher-quality of livability.

Our piece looked at a broader late-2023 context of intensified mergers and acquisitions activity across the homebuilding and major land sellers' firmament. At the same time, we pointed to an M&A-driven hyperbolic growth and earnings strategic arc for UHG itself, given its fully-refreshed and ready-to-deploy capital coffers.

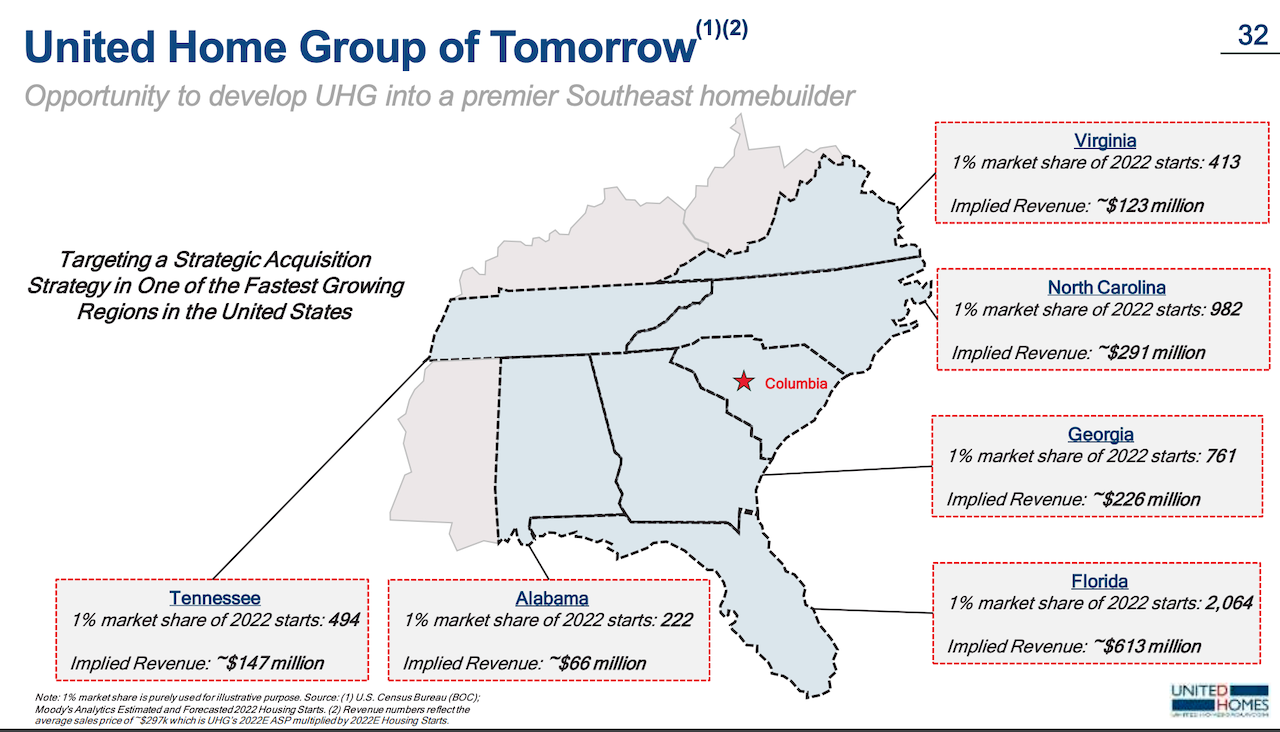

SEC materials the company filed earlier suggest that even a modest 1% market share of new residential real estate and construction activity in each of the seven states UHG plans to enter – Alabama, Florida, Georgia, Kentucky, North Carolina, Tennessee, and Virginia – would catapult the company to 5,000-plus homes with combined revenues of $1.5 billion [based on 2022 figures].

Already, the company has targeted as many as 60 operators currently doing business in the seven-state Southeastern mega-region as potential UHG acquisition opportunities.

We talked at length with recently appointed UHG President Jack Micenko for insight into the M&A game plan, with an eye to adding understanding where and with whom the opportunity-areas stand out the most for a young public with a big appetite and the biggest of ambitions to go with it.

Micenko notes that while land acquisition plays a key underpinning the strategy for accelerated growth, emphasis – with an asset-light approach to owned and controlled lot pipelines – focuses more on finding the right people in the right places with the capability and ambition to build on relationships and reputation, as well as adding product mix-shift and customer segment expansion to UHG's core competency set.

Here are the top 10 nuggets of intelligence Jack – formerly a BTIG Managing Director, Housing Ecosystem Investment Banking – shared with us in a broad and deep conversation on one of homebuilding's most dynamically growing players.

- Footprint

We have this 500-mile radius that we think is important -- from our core market in the Carolinas. We'd like to be in places like Tennessee, Kentucky, and Virginia, as well as to add to North Carolina, add to Georgia, enter Florida at some point. North of Orlando is probably a better fit for our product set."

2. Product set

We're looking at both businesses and product sets. We need to diversify our product offering, particularly in a market like this, where rates have moved so fast. You look at the Toll Brothers' results and they are really strong. So start thinking that move-up buyers are more resilient in the face of affordability issues than others."

3. Product set 2: smaller plans

Product-type -- both consistent product and products that are adjacent to what we're doing -- is a focus. Think about a second move-up type product and a smaller-footprint. We're doing the same organically. We're rolling out smaller footprints. Everybody's everybody's doing that to manage the affordability side."

4. Land-light imperative and land-bank structures

What's important is we're trying to preserve the land-light strategy, so we're not going to take a ton of lots on our balance sheet. Sellers may retain land development as a third-party developer, or they might come work with us. We might buy them in our land business, Pennington, and hold those lots as options through Pennington. But we won't move forward unless it is a land-light strategy for sure. We won't deviate from that."

5. Competition

Look, the bigs have gotten bigger – whether they're big privates or publics – since the GFC. That's not going to change. It's probably only going to increase and accelerate. As banks increasingly focus on their risk-based capital and their exposure -- it's not it's not that they're concerned about the homebuilding industry -- they're concerned about office in their markets, and they're concerned about hospitality. However, that's causing them to make decisions elsewhere in their portfolios. Those decisions are probably not going to be margin-favorable to the smaller privates."

6. Emerging markets

You're seeing big publics in markets that you wouldn't have seen them in three, four or five years ago, ... secondary and tertiary markets. Atlanta – the cat's out of the bag in these bigger Southeastern cities, and it has been for 15-20 years. But, when you look at some of the markets in the Carolinas, outside of Nashville, outside of Atlanta, there's good markets. Some of it's affordability-driven, as Atlanta has gotten expensive. That migration is still occurring. You have to pick your fights. As a smaller builder you have to pick your markets where you can be additive, and where get land. In one of our markets, we've got an LOI out and we're gonna go from seventh and ninth-combined to number four on the land call. It's really local scale."

We have to look at markets where we can do 400 or 500 homes in our line of sight, or else, why are we there? You can have local scale in Greensboro or Fayetteville. Those are decent markets. We've got a list of towns and cities we're looking at. College towns are a great market; large state university towns are a great market. There's a lot of in-migration retired folks moving moved down folks moving to college towns, where the culture and healthcare facilities and overall growth has been unbelievable the last 15 years. There's a lot of that in our market bucket as well."

7. Building a company and driving quarterly earnings performance

This is something that we talk about every day. From the management level to the board level, the question is: 'do you find a larger transformational deal that gets you there quickly, or do you bolt on digestible smaller deals?' There's no right answer; it's all circumstantial. The easy parts getting a getting a deal to the finish line, relatively speaking, the harder part is integration. I worry about the integration side of a large deal relative to smaller deals. I worry about our team's capacity. In some ways, integration is as difficult for small deals, in terms of integrating work-flows, as a big one. It's the same amount of work, whether it's 100 unit acquisition or 1000 units. It's often about the further you get away from your your core base, the riskier it gets. I think the better operationally and the more engaged and committed the merger partner, the better. It has to be right at the human level, because you can't get home for dinner in some of these markets."

8. Timing

We're meeting with a lot of folks. You kiss a lot of frogs before you find any princes. A lot of these folks are just curious as to what we're doing. They might not necessarily be interested in partnering now. Maybe they will be in a year two or three. And so we're as much saying, 'hey, think of us as an option relative to the normal usual list of suspects. Maybe we can be a little more collaborative. Maybe we could look at it more as a partnership with United homes.'

We thought we'd be having conversations with maybe a little bit older folks, who just want to cash out and go take the boat to the Bahamas. That's not really been the case. It's guys that are experienced have a brand, a business, a team, but have kind of hit a ceiling on financing, and they still want to be involved. They still want to be engaged. They see the the opportunity to get in on a public stock basis early on. For instance, if you could have been an early acquisition of a Dream Finders or a Century Communities or an LGI these groups are up 300%, 400%, or 500% from those early years. If we can get more right than we get wrong, there's there's a nice 10-, 12-, 15-year story here. Bringing this team's operational expertise together with the capital market side where I come from, we think we could get a pretty good team on the field to go down this pathway."

9. The private-to-public transition

There's the singular challenge of getting an organization through all levels to think proactively, more as a public, versus reactively, like a private. And there's the challenge of understanding that there are consequences and accountability to be a public company versus a private one. We've been public for a quarter. We're in our infancy stages, but trying to get a mindset of accountability is tougher. Homebuilding is a tough business. Stuff that the team accomplishes today may not affect the business for six or nine months, good or bad. So being proactive and staying on top of that long-tail dynamic of the business is an everyday sort of learning curve transition. We're not the first to go through it and we won't be the last. Every company that makes this transition goes through it. But keeping everybody focused on our numbers, our closings, our start schedules, and all that operational stuff is far more important to get right now than it ever was when nobody was watching."

10. Business cultural fit

Culture is important. Michael Nieri relates to these folks, and they relate to Michael from an entrepreneurial builder-to-builder standpoint. Some of the bigger publics have a very defined box that they put these acquisitions into. We're not defined enough in our operations to have that view. We're looking at at collaborative ideas that make sense. We prefer to have full engagement of the sellers and their teams. We need their people when we move into a new market. Herring Homes was an interesting deal because it reflects more of a 'people deal' and a market intelligence deal than a 'we-got-some-lots-and-we got-some-forward control.' A lot of it is going to be giving Brian the capital he needs to go find stuff that makes sense in those markets. You're much better doing that with a guy that's been on the ground there for 25 years than to put your own people there and see them make mistakes that could be avoided."

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Capital

Tariff Shock Tests Homebuilders M&A Pipeline, Capital Access

Despite market volatility and policy whiplash, key homebuilding deals continue to close. Builder Advisor Group doubles down on financing muscle as banks pull back.

Steel, Skeptics, And The Real Innovators In U.S. Homebuilding

TBD MasterClass contributor Scott Finfer shares a brutally honest tale of land, failed dreams, and a new bet on steel-frame homes in Texas. It's not just bold — it might actually work.

Housing’s High-Stakes Year: Six New Home Market Shifts To Watch

A massive liquidity crunch is reshaping homebuilding’s financial landscape. M&A is accelerating as builders chase capital and growth.