Leadership

Pictures Tell Stories: This Chart Is A Housing Market Cautionary Tale

Demographics – namely, the magnitude of Millennial and GenZ adult households and Baby Boom movers – may add up to a decade or more of new-home demand. Maybe don't bet on a smooth trajectory.

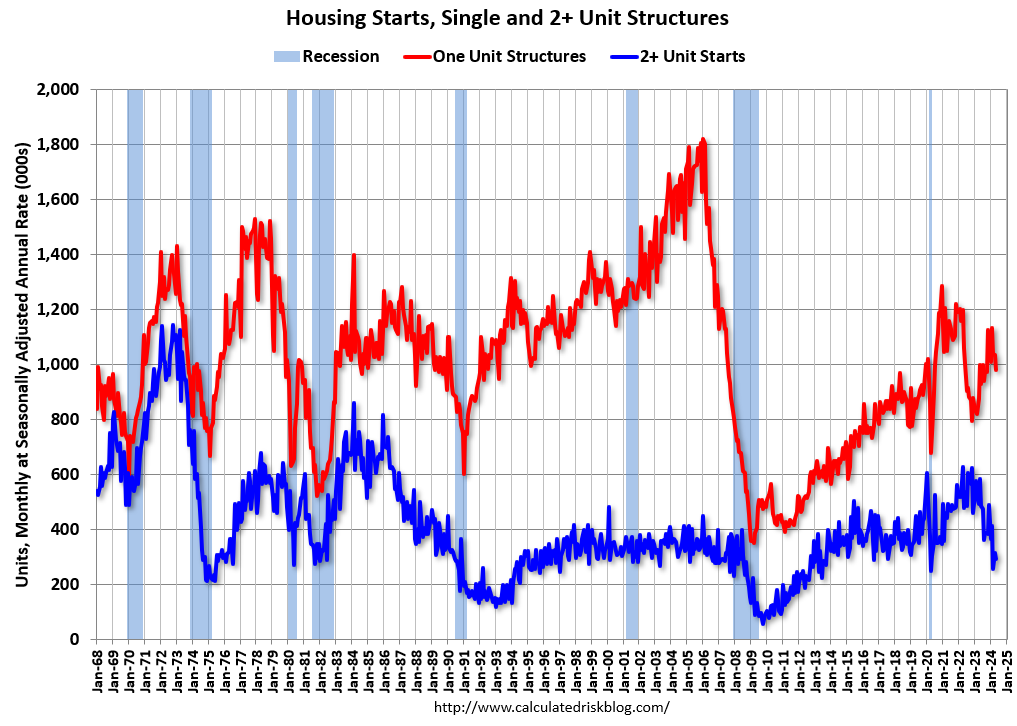

The context of the picture below is today's release of monthly Census data on new U.S. housing production – single- and multi-family starts, building permits, and completions.

They say a picture's worth a thousand words, and this one speaks volumes. We'll come back to that, but first ...

In Bill McBride's words, here's what the picture describes:

This shows the huge collapse following the housing bubble, and then the eventual recovery - and the recent collapse and now recovery in single-family starts."

[Calculated Risk's Bill McBride is a student of the meaning and direction of these numbers and can be counted on as a teacher for many of us who need guidance on what to look for, what the numbers mean, and why they matters. So, please, if you don't, subscribe to his Substack site.]

The thousand words this picture is worth to me is less about the brief time period most business leaders in homebuilding and residential development and investment are looking at – the 2019 pre-pandemic "normal" to a post-pandemic "new normal."

Rather – in light of the pain, frustration, anxiety, and growing ire I hear from homebuilders, especially those who lead companies financed with their own resources, and bank lending, and private investors – I look at the picture's right-hand quarter and the chart's left-hand third and wonder... and we'll come back to that, but first ...

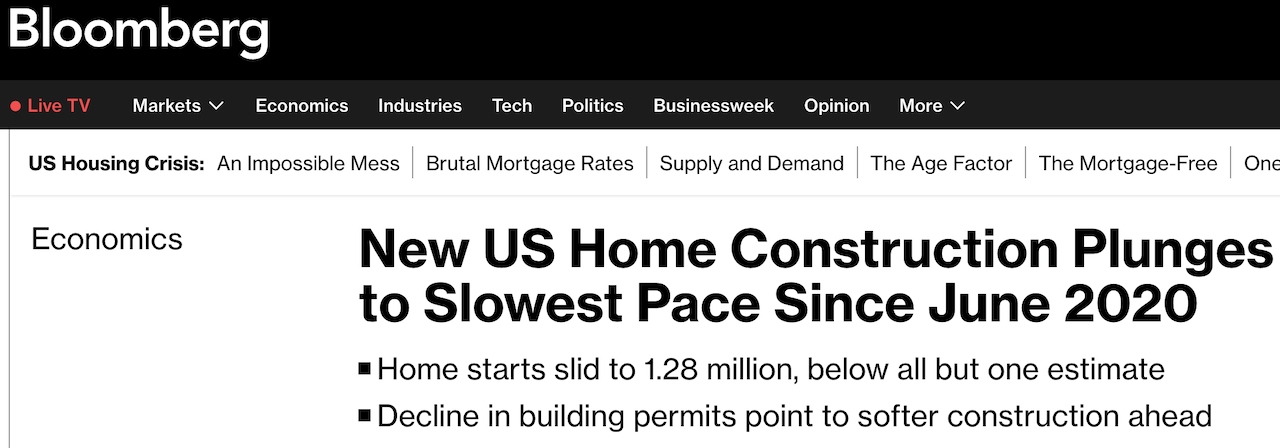

Today's housing starts release came in below expectations and contain its own story of an industry community struggling mightily and striving to maintain its footing. This, despite the best efforts of the nation's central bank to weigh heavily against success and thriving in the business of new-home production.

Here's one perspective from the business media point of view:

Bloomberg housing and real estate correspondent Michael Sasso writes:

New home construction in the US slumped in May to the slowest pace in four years, as higher-for-longer interest rates sap the housing industry’s momentum from earlier this year.

Housing starts decreased 5.5% to a 1.28 million annualized rate last month, according to government data released Thursday. The figure was below all but one estimate in a Bloomberg survey of economists."

Robert Dietz, chief economist for the National Association of Home Builders, takes a less hyperbolic tone in his reading of today's data release, but aligns in general with Sasso's take-aways:

Single-family and multifamily housing starts fell in May as high interest rates for construction and development loans and elevated mortgage rates held back both housing supply and demand.

Overall housing starts fell 5.5% in May to a seasonally adjusted annual rate of 1.28 million units, according to a report from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau.

The May reading of 1.28 million starts is the number of housing units builders would begin if development kept this pace for the next 12 months. Within this overall number, single-family starts decreased 5.2% to a 982,000 seasonally adjusted annual rate. However, on a year-to-date basis, single-family starts are up 18.8%, albeit off weak early 2023 data. Mortgage rates averaged 7.06% in May per Freddie Mac, the highest reading since November 2023. This high interest rate environment is causing many potential buyers to remain on the sidelines."

A third view, and one that unpacks some of the more salient near- and mid-term implications for home builders comes through in Wolfe Research senior analyst Truman Patterson's telegraphic take-aways from the data points:

SF Starts have fallen below the 1M mark for the first time since Oct ’23. With SF Permits now below 1M for three consecutive months, we expect SF Starts will remain below 1M over the near-to-intermediate term. Clearly, decelerating construction activity should not be surprising given the increase in mortgage rates above 7.0% combined with the 2 point drop in the HMI yesterday (6/19) to 43, which indicated the New Housing market is firmly back in contractionary territory (MoM). With completed New Home Inventory up 14.1% since January, we applaud the SF S&P decline, which should help mitigate home price discounting to a degree (mortgage rates now back below 7% also help). That said, we note our May Private Homebuilder Survey (link) indicates that 60% of builders believe consumer expectations for a 2H Fed rate reductions is an impediment to current New Home demand, indicating summer demand could face headwinds despite the recent rate retrenchment."

Note that Patterson sees housing producers' reining in of new starts as a business positive, since otherwise, they may enter into greater risk of over-building into a lower demand environment, which would mean having to offer greater discounts and margin-crushing incentives to keep new orders coming in.

Those are the running and relevant expert perspectives on today's starts and permits release.

But I keep on thinking of the mounting pain, frustration, anxiety, and ire among homebuilding owners and leaders. They're stuck between a rock of protracted local community obstacles, impediments, delays to putting new lots on the ground for home development, and the hard place of local, regional, and even national banks closing down their acquisition and development activities until further notice.

Land development, acquisition, financing, and frontline worker labor hours and materials are tightening, squeezing, and spiraling higher at every turn for builders. Trying to stay hitched to as many household incomes as they can to remain in a relative attainability range.

We can only reduce the cost of housing by increasing productivity through efficiencies of our operation," Lennar executive chairman Stuart Miller told analysts this week as he contextualized Lennar's Q2 2024 earnings performance.

The defining story of homebuilding in the 2020s is right there. How will homebuilders accomplish what Miller says has to happen?

Now, no homebuilder runs their business with national housing starts and permits data as a meaningful operational KPI. But if you look at the left-hand side of Bill McBride's almost 50-year chart, and you see both a stark contrast and a blast of deja vu.

The stark contrast is that by and large, in the 1970s, '80s, and '90s, through 2005, housing starts ran at a level that eclipses the last 14 years by a mile. That's despite a sizable population increase and the emergence of Millennials a decade ago into what should have been their hyper-active embrace of homeownership.

So we see from that image that homebuilders have contended with shackles since the Global Financial Crisis.

However, if you look at the four red fever chart line dips on that left-hand side – in 1970, 1974-75, 1980, and 1981-84 – there's a thousand words there that may apply to conditions and scenarios in today's housing market.

The big take-away in those thousand words is that we can not rely solely on age and cohort demographics – namely, the magnitude of Millennial and GenZ adult households – as a sure-bet to predictable demand.

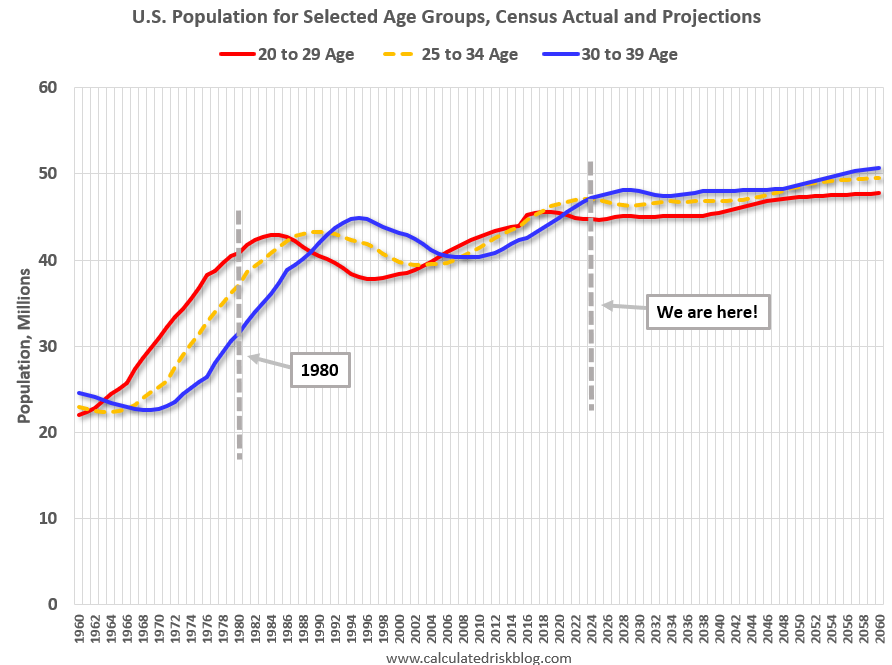

Another Bill McBride analysis and picture helps show that clearly: Comparing the Current Housing Market to the 1978 to 1982 period

A couple of McBride's notes on this data:

For buying, the 30 to 39 age group (blue) is important. The population in this age group is increasing and will increase further over this decade.

When we look back at the 1978 to 1982 period, the 30 to 39 age group (blue) was increasing even more than today (supporting house prices).

Part of the issue is this. The "pig in the python" size of the Baby Boom generation and their job-, household-, and family formation patterns didn't prevent two or three dramatic housing and economic downturns.

While Millennials and their leading-edge GenZ successors will drive the overall market in a positive direction for the next decade at least, it won't be a smooth ride.

That's it in 1,341 words.

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Leadership

10 Bold Ideas Tackling Housing Affordability And Access Now

From AI to hempcrete, these 10 ideas show how innovation in design, finance, and policy can open the door to housing affordability.

Sumitomo Forestry Sharpens U.S. Focus With DRB Move

Strategic clarity replaces portfolio sprawl as Sumitomo bets big on U.S. scale and integration.

Homebuilders and Insurance: A New-Reality Cost To Stay Ahead

Exclusive insights from Westwood Insurance Agency’s Alan Umaly and MSI’s Naimish Patel reveal why homebuilders must rethink insurance, resilience, and risk management—or risk losing buyers in an increasingly volatile market.