Leadership

Backlog Logjam May Dampen Spring Selling: Deja Vu All Over

2022's word-of-the-year for homebuilders and their partners: Capability. And in most cases, that means deep pockets, deep local scale, and deep relationships with vendors.

Going back, a Roman calendar date got colored red to set it off from the dates in black ink if it was to stand out in importance, mostly to mark observance of a feast day, a holiday, or a festival time.

By all rights, Friday, Feb. 18, 2022 should mark a red letter day for homebuilders and their partners, at least as a symbolic watershed signifying the new year's Spring Selling season.

It's a time – typically -- of manicured landscapes, pristine entry-scapes and dazzling new monuments, sculpted hardscapes, new elevations, adaptive new floor-plans, fresh paint, ribbon cuttings, community center galas for real estate agents and their clients.

In today's fevered, out-of-whack, liminal time of surging demand versus relatively trickly supply, the date would likely signify lots and lots of earnest money deposits, long "interest lists," and outright full cash offers on the spot.

Instead, between now and that date just over a month from now, what happens in those next 30 business weekdays will reveal a great deal about whether 2022 can look, feel, and behave differently than the year just past or not.

Omicron, the more-cunning, presumably less-lethal variant of the COVID-19 virus continues – if nothing else – to smash predictability models when it comes to people being able to count on getting their jobs done on any given day.

As much as the business world, society, and culture desire, want, need, and determine that normalcy prevail – and that includes the tens of thousands of supply chain linkages that need to occur to produce a normally designed 2,200-square feet, three-bedroom new home – the natural history of Covid still runs the show, for all intents and purposes.

Despite a strong economy from an above-the-K curve consumer household spending and means perspective, and despite a demographic arc that common sense would argue that "you ain't seen nothin' yet" on the household formations and reformations front, and despite interest rates, even after a Fed liftoff, making now the moment to move, and despite soaring rents and tight vacancies among the nation's larger landlords, ... despite all of this, the year that homebuilders and their business partners across a wide spectrum 0f industries, product categories, and related services expect to have in 2022 may look more like 2021 than they'd all like.

An overarching view – given the way access lines to capability on both the building materials and products front and on a skilled workforce whose capacity doesn't match up to the predicted flow and expectations of new housing activity – is that clout, heft, local scale, market concentration, and regionalized inventory stocking will continue to advantage the biggest 50 or 75 homebuilding enterprises over upwards of 4,900 smaller firms who build and sell as many as 9 out of every 10 new homes.

The 2022 Word of the Year in Homebuilding: Capability

Capability – which wraps together holding a competitive edge in access to constrained materials and building products, a nimble and ready sway with as many as 25 subspecialty contracting trade crews, strong ties to local inspection officials, and a big checkbook to pay surge pricing upfront in hopes of later recouping the budget variances to the balance sheet by passing the costs to the buyer – is the word of 2022 for homebuilders.

Near-term, capability, which is not a given, nor an even-handed alternative for homebuilders of different sizes, local activities, vendor relationships, capital lines, etc. – will determine how soon builders can finish work that they'd pencilled for 2021, and get moving on even more work they're gearing up to do in 2022.

Capability, as well, will impact the degree to which builders can work-around ongoing disruptions to the chain as they attempt to kick-start selling, open new neighborhoods, and drive greater volumes.

The timing of which companies have the wherewithal to secure capability versus those who need to scrimp and struggle for it looms large, even as price-tag pressure intensifies and the wildcard of interest rate increases seizes at least some of current would-be buyer prospects and pulls them out of monthly-payment contention unless they can keep pace with the impacts with increased take-home wages.

Vaunted materials price spikes – like the nearly $18,600 lumber bump to new home prices thanks to the one-two combo of seasonal-and-pandemic impacted supply-demand dynamics – will hurt, and potentially deeply harm, firms with more limited optionality on timing, capital, and access to resources, than it does those with deeper pockets, bigger sway, and more room to maneuver on the capital structure front. That's not just because the prices will need to go up to match cost, but because materials and products allocations they can get their hands on may crimp their construction pace for a second year running, further straining their more restrictive access to capital financing.

Wall Street Journal staffer Nicole Friedman set up the context of a weighty – potentially perilous -- hangover that started in 2020 and intensified in 2021, and shows little sign of easing amidst promises of a large push of new activity to offset the backlogs and unfinished completions budgeted by year-end. F:

Many builders so far have been able to pass increased material costs along to home buyers. But with home prices higher than ever—the median price of a newly built home in November rose 18.8% from a year earlier to a record $416,900—some builders are concerned about pricing out potential buyers.

Builders are scrambling to find new suppliers, stock up on building products and use substitute materials. Some are scouring retail big-box stores for products they can’t find through the normal supply channels.

Friedman notes in her story that homebuilders' backlog of new single-family homes currently under construction had surged 28% in November 2021, to the highest seasonally adjusted level since 2007 as measured by the Commerce Department. That number very likely increased in December.

So, when Spring Selling begins – even symbolically – will it really begin, or will the moment feel depressingly like it did a short way into 2021, when sellers had to shut down sales, stop taking names, and start treading water during long limbo of invisibility into how long it would take to build what already had been sold?

Inflation and interest rates' impact on buyer behavior, and ongoing supply chain disruptions to scheduling and completion operational models are already the known challenges to plan.

To the best of their ability to model, here above is a snapshot of the challenge roadmap for anybody working through a hangover backlog, trying to clear it to get ready for a fresh pipeline of Spring Selling orders.

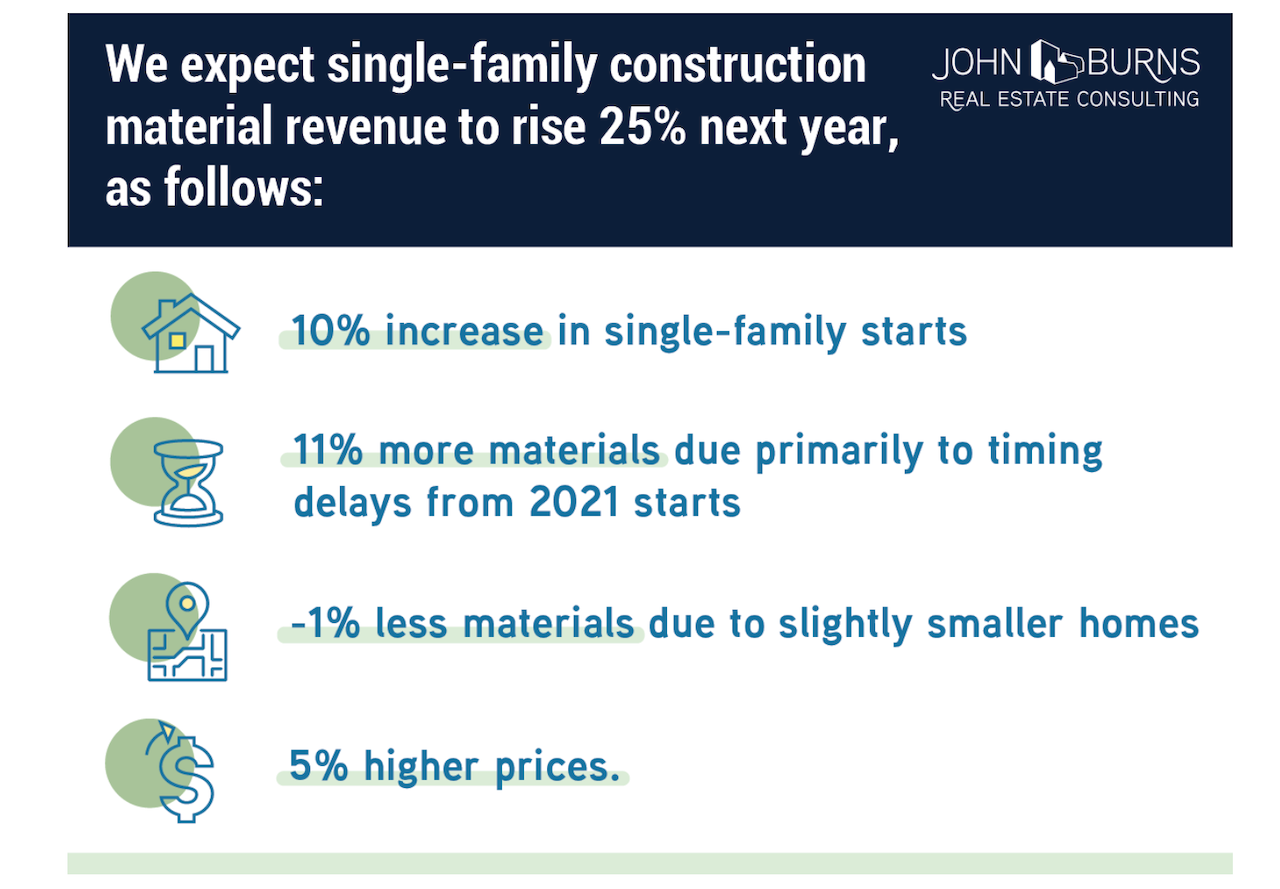

John Burns Real Estate Consulting principal Todd Tomalak notes:

We think material demand could grow by 20%+, even with starts growing 10%. Price hikes will add another 5%, increasing total single-family construction material demand 25%. This will be greater than the 10% increases in total residential spending dealers reported to us this year."

The additional demand is the result of the extended time it takes to build a home, which is causing builders to install materials later in the cycle. This will vary a lot by material of course because the builders are also ordering some materials earlier than usual due to the shortages. To make things worse, dealers in our survey appear to be planning (and buying inventory) based on an expectation of far less growth than we expect they will see."

Ultimately, it's omicron and possibly a variant of Covid we haven't yet all heard the name of that will determine whether this year's Spring Selling Season will be all that it's cracked up to be.

One way or another, the pressures of how those 30 days tick down to Feb. 18, and what they mean for builders' capability – skilled people, the right materials, and flexible, patient capital, together with a highly-motivated but tolerant buyer – will weigh more heavily on smaller players in the community than those whose capital structures are built to withstand turbulence.

Fasten seatbelts. That red ink may mean something else come the outcomes of the next four to eight weeks.

Join the conversation

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Leadership

10 Bold Ideas Tackling Housing Affordability And Access Now

From AI to hempcrete, these 10 ideas show how innovation in design, finance, and policy can open the door to housing affordability.

Sumitomo Forestry Sharpens U.S. Focus With DRB Move

Strategic clarity replaces portfolio sprawl as Sumitomo bets big on U.S. scale and integration.

Homebuilders and Insurance: A New-Reality Cost To Stay Ahead

Exclusive insights from Westwood Insurance Agency’s Alan Umaly and MSI’s Naimish Patel reveal why homebuilders must rethink insurance, resilience, and risk management—or risk losing buyers in an increasingly volatile market.